How the Iran War Is Accelerating the Race for Critical Minerals

The world is rushing to escape fossil fuel dependence, leading to a new race over the inputs that drive clean energy

The New Dependency

As the world moves into the hot summer season, eyes on the Strait of Hormuz are intensifying. Since the Iran crisis began, roughly 20 million barrels a day—about 25% of global seaborne oil—has been choked off. Reuters reports cumulative losses having reached 624 million barrels over 52 days, a figure that staggers even seasoned energy analysts.

Even as hopes rise for an end to the crisis amid Pakistan-mediated peace talks, the systemic ripple effects will last years to come. Fatih Birol, the executive director of the International Energy Agency (IEA), has been unambiguous: the “damage is done.”

The immediate casualties are well-documented: oil above $120 a barrel today, freight costs surging, insurance markets seizing up. But the more consequential story may be what the crisis is doing to the energy systems built to replace oil.

For decades, those who championed renewable energy warned that continued dependence on fossil fuels would eventually produce a calamity like this. Governments across the world are now listening.

The UK announced a March 15 package of clean energy measures, including the introduction of “plug-in” solar panels, explicitly framed around combating energy insecurity. In China, which dominates the global solar industry, exports doubled in March alone, reaching 68GW, according to CGTN Europe.

The market logic has shifted. The energy transition is no longer driven primarily by climate consensus. It’s now driven by something governments find easier to sell: national security.

But there’s a problem embedded in this pivot: the clean energy system isn’t resource-independent, either. Solar panels, wind turbines, and electric vehicles all require copper, lithium, cobalt, and rare earths at enormous scale. Critical minerals accumulate in infrastructure, and that infrastructure has to be built, replaced, and expanded continuously.

The numbers are striking. The IEA projects critical mineral demand growth of 3.5 times current levels by 2030, with lithium alone potentially requiring 40 times today’s supply. The U.S. Geological Survey projects global demand for key critical minerals to increase by 400-600% by 2040 to support clean energy technologies. These were already steep curves before the Iran war; the crisis is steepening them further.

The New Scramble

The backdoor dealmaking has already begun and the pace is accelerating. USA Rare Earth recently completed a $2.8 billion acquisition of the Brazilian rare earth mine Serra Verde. The US and India have announced a joint partnership to restart copper and cobalt mine production in the Democratic Republic of Congo. The message being signaled: mineral security is now as urgent as energy security.

Gulf countries, despite experiencing mounting fiscal pressure from the Iran war, aren’t sitting out of this race. More than a week into the war, American investment firm Cove Capital and Saudi conglomerate Abdel Hadi Abdullah Al-Qahtani Group of Companies (AHQ) announced a joint multibillion-dollar fund to invest in critical mineral projects across Africa. Capital that might have retreated is instead being redeployed toward the next strategic frontier.

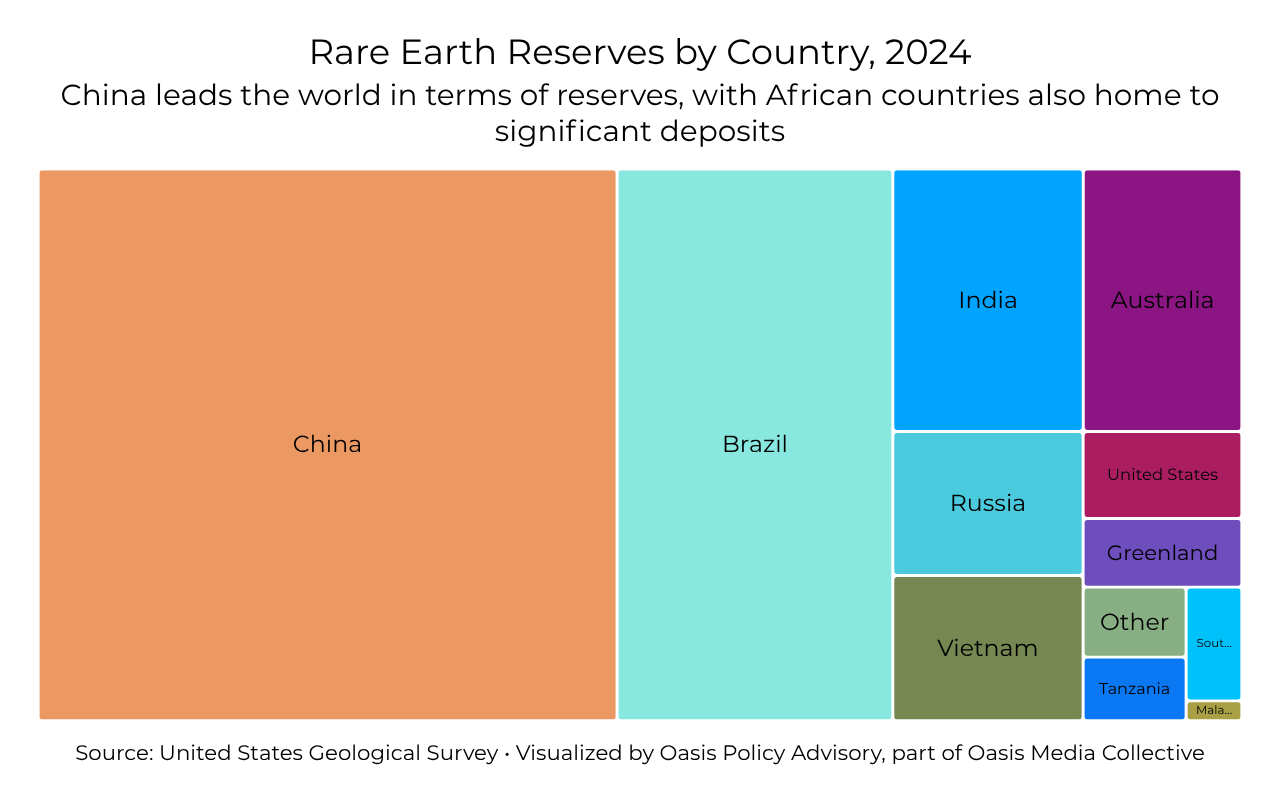

That frontier is increasingly African. The continent holds approximately 30% of the world’s known critical mineral reserves and is projected to supply 10% of global rare earths by 2030, alongside dominant shares of cobalt and manganese.

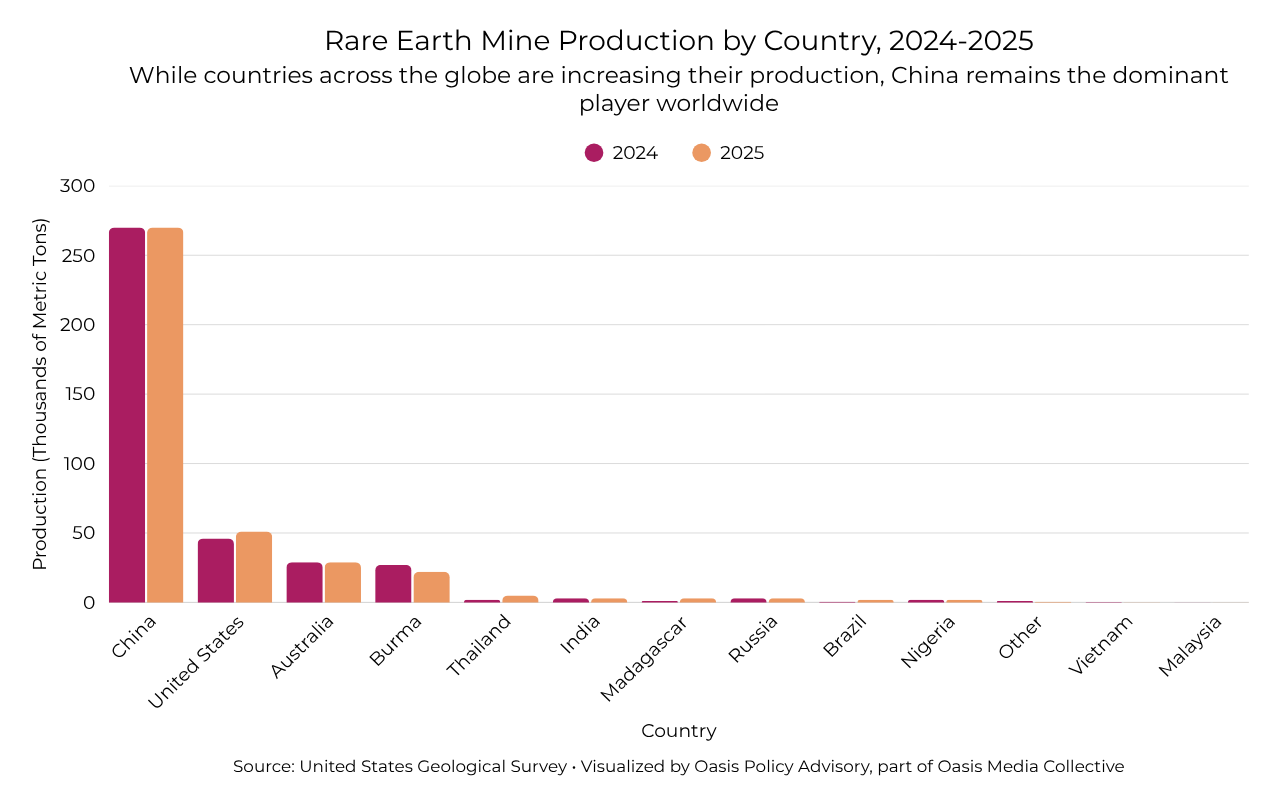

Meanwhile, China’s structural position complicates every Western and Gulf strategy. Controlling approximately 90% of rare earth processing globally, Beijing’s leverage over the energy transition doesn’t depend on owning the mines. Its doubling of solar exports in March is a signal of that: the transition is accelerating and China intends to be the one supplying it.

The oil concentration that defined the Gulf’s geopolitical power for over half a century may, over time, give way to mineral concentration across the mines of the DRC, South Africa, and beyond, with processing power anchored, for now, in China.

That’s a trend the Iran war most certainly did not start. But it has accelerated it, loudly and irreversibly.

This reporting may be cited with attribution to Oasis Media Collective. For licensing, republication, or extended use, contact here.