Your Coffee Is Already Expensive. A War in East Africa Could Make It Worse

The geopolitical crisis that could push your favorite Starbucks order past $10

KEY QUESTIONS

WHAT HAPPENED? Coffee prices are seeing historic highs just as tensions between Ethiopia and Eritrea escalate over Red Sea access

WHY IT MATTERS? Ethiopia is one of the world’s largest exporters of coffee, and conflict could disrupt global supply chains, sparking price hikes

WHAT’S NEXT? If war erupts, the world could face anywhere from modest Arabica price premiums to a loss of millions of bags from global supply

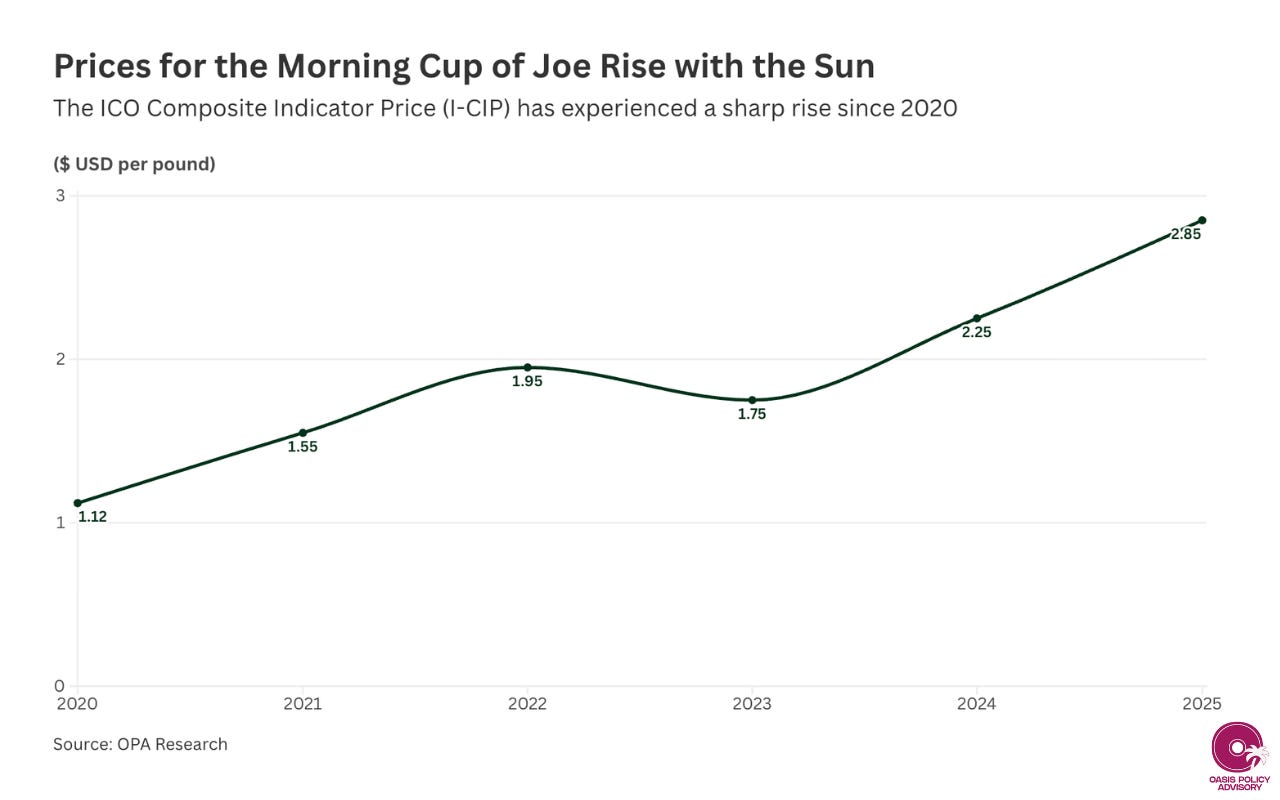

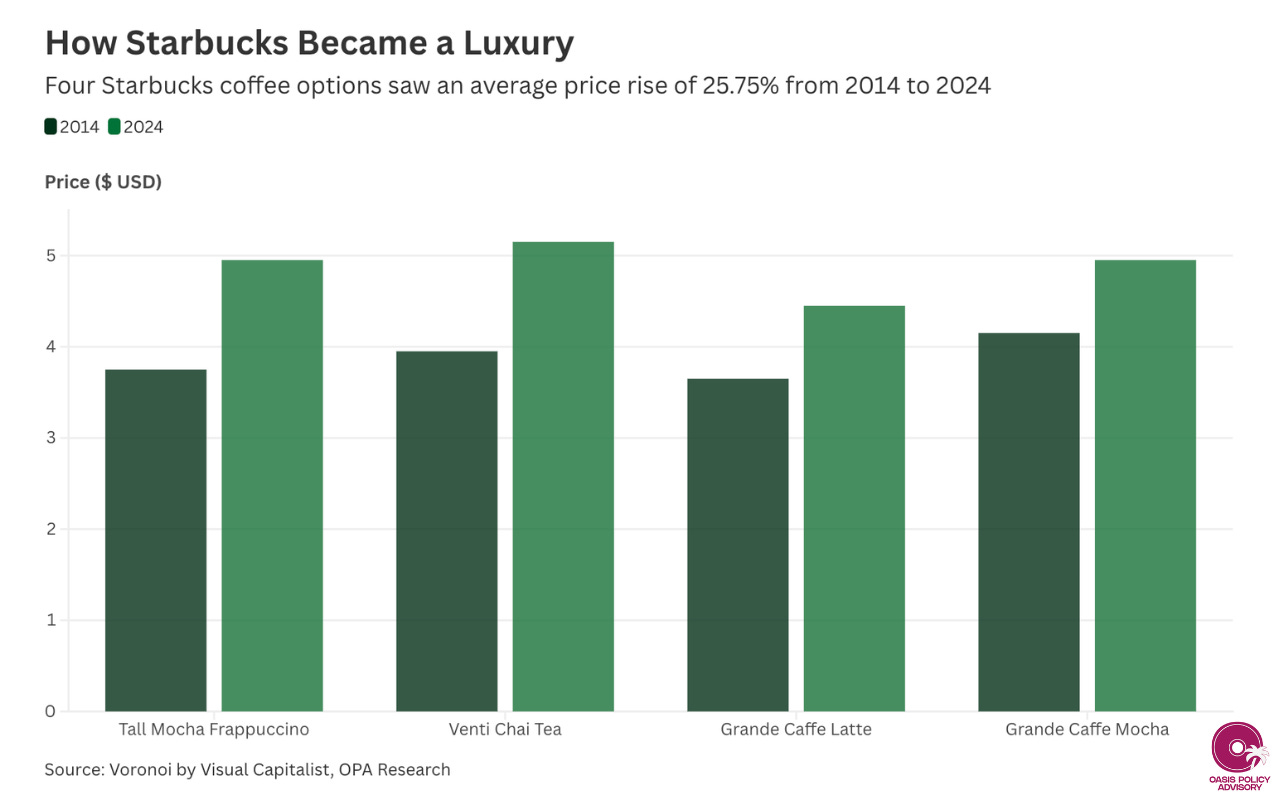

If your morning cup of joe has started feeling like a luxury, you’re not imagining it. Coffee prices have approached historic highs of 325 cents per pound in 2025, according to the International Coffee Organization (ICO). Starbucks’ Tall Mocha Frappuccino jumped from $3.75 in 2014 to $4.95 in 2024, a 32% increase; my personal favorite, Venti Caramel Macchiato, similarly rose 17% over the same period.

For coffee lovers living paycheck-to-paycheck, they’re left wondering what’s driving this rise. Global inflation plays a role, but an under appreciated driver are geopolitical shocks to the supply chains underpinning coffee prices. And another one is now taking shape in the Horn of Africa.

Neighbors Ethiopia and Eritrea are edging toward conflict, with Addis Ababa seeking Red Sea access through Eritrea’s port city of Assab. For global coffee markets, already stretched thin, the timing could hardly be worse.

The Producer Behind Your Morning Coffee

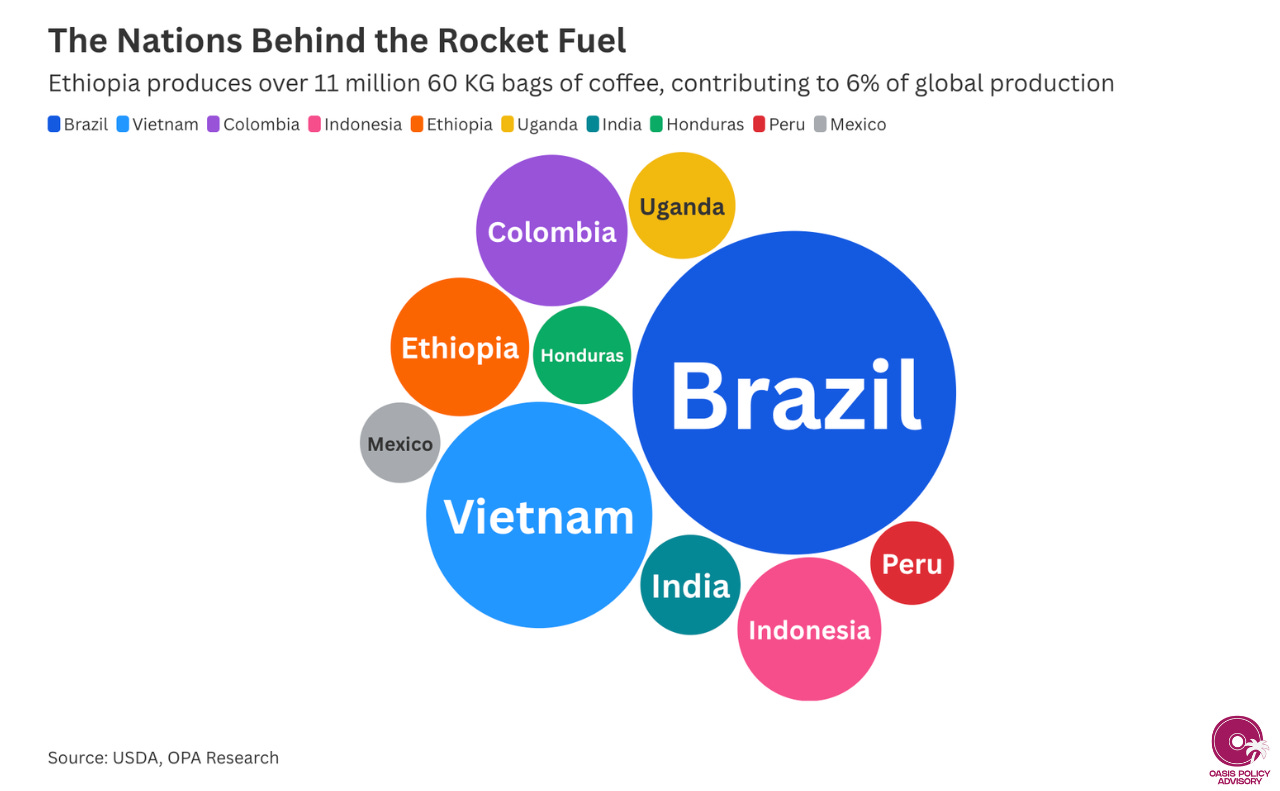

Ethiopia is the world’s fifth-largest coffee producer and third-largest exporter of Arabica, the bean that accounts for roughly 60% of global production. In 2024/25, the country exported $2.65 billion worth of coffee, a 21.5% year-on-year increase, supplying premium beans to Saudi Arabia, Germany, and beyond.

Yet Ethiopia’s dazzling numbers have a kryptonite: Djibouti is its sole maritime gateway, connecting Ethiopian coffee to global markets via the Red Sea. That chokepoint was already severely stressed by the Houthi campaign in the Red Sea in 2024. Before the crisis, at least one vessel arrived daily in Djibouti; that fell to one per month at its worst, according to trade intelligence platform Tridge. Royal Coffee’s 2024 logistics update similarly reported that export capacity from Djibouti was cut by half. Ethiopia’s supply chains are as fragile as they are impressive.

Some will point to the Tigray War—a civil war that erupted in Ethiopia’s northern Tigray region from 2020 to 2022—as reassurance that conflict won’t disrupt coffee exports. Despite the war’s devastation, Ethiopia’s main coffee-producing zones in the south kept functioning, and exports actually rose: Bloomberg reported 86,000 tons shipped in the three months to October 2021, a 77% increase on prior estimates.

But a war with Eritrea would be a different beast.

Three Roads to Disruption

Diverging paths lie ahead for the Horn. While varying in their intensity, all three threaten volatility to coffee markets.

Border Skirmishes: Noise Without Signal

Localized clashes, contained in the north along the Ethiopia-Eritrea border and away from the southern coffee-producing regions of Oromia and Sidama, would leave physical supply largely intact. Market impact would be driven more by ESG anxiety than security shocks over humanitarian and reputational concerns regarding the war.

Drones, Railways, and Economic Warfare

A full-scale confrontation raises far graver risks. While ground fighting will remain concentrated in the north, the real risk is elevated in the skies. East Africa has become awash with drone warfare, used extensively during the Tigray conflict by both Addis Ababa and Asmara and in the ongoing Sudan war, to strike deep into rival territory. Eritrea could target Ethiopia’s southern coffee regions, knowing the industry underpins 30-35% of the country’s export earnings and supports 15 million people. More critically, the Addis Ababa-Djibouti Railway—which carries roughly 25% of Ethiopia’s exports—would be a prime target. Its effective shutdown could cost over two million bags in a single season.

Red Sea in the Crossfire

The most severe scenario. Assab sits adjacent to the Bab el-Mandeb strait, having been the world’s most disrupted shipping lane in 2024. Fighting near or around it would compound looming Houthi-driven volatility, spook carriers further, and potentially reduce Ethiopian export capacity by 50%, erasing over 2 million bags from global supply. Freight costs and insurance premiums would spike, pushing coffee prices sharply higher regardless of what happens on the ground.

The Bigger Picture

This isn’t just about one conflict. Coffee has become increasingly exposed to overlapping, simultaneous shocks: Brazilian drought, Indonesian climate stress, and now a potential Horn of Africa war. Each alone is manageable. Together, they point to a commodity whose supply chains are structurally fragile.

As sourcing grows more precarious, the question facing roasters, retailers, and everyday consumers is no longer whether diversification is needed, but whether it’s already too late.

This reporting may be cited with attribution to Oasis Media Collective. For licensing, republication, or extended use, contact here.

It won’t be gas prices that tip the scales of US politics this year