The Red Sea’s Next Crisis Is Already Forming

Sudan’s expanding war, Ethiopia’s push for ports, and the hidden risks facing East Africa’s blue-economy boom

Welcome to the February edition of Oasis Media Collective’s flagship Investigations series, where we provide a deep dive of emerging yet overlooked trends upending the world today.

Since the 18th century, global and regional powers have long marveled at the Red Sea, a critical maritime corridor through which roughly 12% of global trade passes. From the British Empire’s incursion into Egypt to the French Empire’s conquest of Djibouti, nations near and far have long sought influence along this vital inlet.

It was for this reason that 2023 felt like a blast from the past for blue economists. The Houthi campaign against maritime shippers prompted an international trade crisis, leading to a 30% rise in container freight rates, an average two-week increase in shipping time, and costing countries like Egypt a total of $7 billion.

With the Houthis having declared an official end to their maritime campaign, many regionally and globally are taking a breadth of fresh air.

But the Red Sea crisis is far from finished.

Paralleling Yemen to the West is the Horn of Africa, one of the most strategically vital regions in the world—and among the most unstable. The convergence of three escalating regional conflicts threatens to kickstart a new maritime crisis. Yet this time, the victims won’t be the shipping giants traversing the inlet. Rather, it will be the region’s burgeoning bluetech sector, as they face new geopolitical risks they lack the resources to maneuver, and a new bloc-based funding calculus that replaces the traditional market-based logic they are accustomed to.

Three Converging Flashpoints

Three regional flashpoints are growing in the Horn that spell trouble for the Red Sea, each carrying specific, escalating risks for the region’s geopolitical and investment landscapes:

War in the Skies, War on the Coast: The Sudan Conflict

In the aftermath of Ethiopia’s invasion of Somalia in 2006, an insurgency raged that quickly expanded eastwards to the Red Sea. Mirroring the Houthis’ 2023 campaign, Somali militants discord arose off the coast, targeting any and all merchants that traversed there. The escalation of the Sudan conflict risks turning it into the new Somalia.

Increasingly, both the Sudanese Armed Forces (SAF) and the Rapid Support Forces (RSF) have relied on drone warfare to target each other across the country. The most significant escalation occurred last May, when the RSF struck the coastline city of Port Sudan, the then SAF headquarters and de facto administrative capital of the country. The city’s international airport, a fuel depot, and the Osman Digna Air Base were among the targets.

While the strikes did nothing to immediately deter maritime trade or weaken port operations, blue economists should see it as a cautionary tale: the war’s theater now includes the Red Sea coast, threatening navigation safety.

Not only are armed belligerents eyeing Sudan’s coastline, but also foreign powers. Russia has long sought to expand its naval footprint worldwide; the Sudanese Defence Ministry is reportedly in discussions with Moscow to receive Su-30 and Su-35 fighter aircraft in exchange for a Russian naval base in Port Sudan. Similarly, reports emerged last year of the SAF deploying Iranian drones, including the Mohajer-6, which analysts argue was decisive in retaking Omdurman. In exchange, Iran requested a naval base in Port Sudan.

The presence of both Russia and Iran in Sudan poses a clear security threat that could draw Western-aligned forces into a proxy confrontation. Following the war’s onset in 2023, the Wagner Group quickly emerged as an ally to the RSF; this has been countered by Ukrainian special forces operating in Sudan, with footage showing the interrogation of a Wagner prisoner and Ukrainian kamikaze drone strikes against RSF forces. If Russia and Iran gain a maritime foothold, it may prompt the redeployment of Ukrainian special forces (no longer allied with the SAF given its ties to the Kremlin), but acting independently to target naval operations.

The expansion of the conflict to the coast with various domestic and foreign actors involved holds direct financial implications. For investors in port logistics, fishery processing, or other infrastructure ventures along the Red Sea coast, the use of advanced drone warfare signals a massive increase in asset-impairment risk. This instability renders physical assets virtually non-investable and poses a near-total exit risk for early backers who have no stable counterpart to negotiate with or whose operations are permanently suspended.

Struggle for the Nile: The GERD Dispute

Announced in 2011, the Grand Ethiopian Renaissance Dam (GERD) is located near the Blue Nile River in Ethiopia’s western Benishangul-Gumuz region. The GERD is expected to be Africa’s largest hydroelectric facility, capable of holding up to 74 billion cubic meters of water and generating over 5,000 megawatts of electricity.

Officially inaugurated in early September and reaching full reservoir capacity, the GERD has become a point of contention in relations between Egypt, Ethiopia, and Sudan, with Cairo and Khartoum viewing it as a concern to downstream water flows upon which both countries depend.

The GERD dispute exemplifies a massive resource and long-term regulatory risk for investors. Any VC or PE firm backing agritech, water purification, food processing, or large industrial enterprises in or around the Nile Basin must treat the GERD as a critical factor in their financial modeling. The outcome of the dispute directly dictates:

Utility Price Structure: Whether power and water are stable and affordable or scarce and expensive.

Viability of Water-Intensive Ventures: The political gridlock makes long-term resource security unpredictable, rendering water-intensive ventures in downstream countries exceptionally high-risk.

Ethiopia’s Red Sea Ambitions and the Bloc-Based Funding Calculus

Yet, the Nile is just one pillar of Ethiopian Prime Minister Abiy Ahmed’s economic ambitions; the other is the Red Sea. As the capital of the world’s most populous landlocked country, Addis Ababa has long aspired to regain access to the sea, a strategic imperative that contributed to Ethiopia’s annexation of Eritrea in 1962. Since Eritrea’s secession in 1993, Ethiopia has been dependent on Djibouti for 95% of its seaborne trade, at an annual cost of $1.5 billion.

Seeking to reduce this dependency, Ethiopia signed a controversial agreement with Somaliland’s breakaway government in 2024. Under the memorandum of understanding (MoU), Somaliland would lease approximately 19-20 kilometers of Gulf of Aden coastline to Ethiopia for commercial and naval use over a 50-year period. In return, Addis Ababa would commit to an “in-depth assessment” of formally establishing diplomatic ties with Somaliland, an arrangement that Somaliland officials hailed as a breakthrough. Then Somaliland President Muse Bihi Abdi stated:

“Today, it is with immense pride, I announce the mutually beneficial agreement between Somaliland and Ethiopia. In exchange for 20km sea access for the Ethiopian Naval forces, leased for a period of 50 years, Ethiopia will formally recognize the Republic of Somaliland, setting a precedent as the first nation to extend international recognition to our country.”

The MoU drew a sharp rebuke from Somalia, which recalled its ambassador to Ethiopia and passed a legislation nullifying the agreement.

Although Turkey later brokered a mediation process in December 2024 aimed at easing tensions between Addis Ababa and Mogadishu, Ethiopian Prime Minister Abiy Ahmed has continued to reiterate that Red Sea access remains non-negotiable for Addis Ababa. “The Red Sea was in our hands 30 years ago,” Abiy said. “That history was yesterday’s mistake. Tomorrow it will be corrected. It is not too difficult.”

These remarks have reignited tensions with neighboring Eritrea, as Ethiopian officials have suggested the possibility of regaining maritime access through Eritrea’s port city of Assab.

“The question now is not whether Assab is ours or not, but how we get it back,” Ethiopian Ambassador to Kenya and retired General Bacha Debele said in an interview on November 3.

In response, Eritrea formally withdrew from the Intergovernmental Authority on Development (IGAD), East Africa’s regional bloc, on December 12. In a statement, Asmara accused IGAD of having “forfeited its legal mandate and authority” and failing to uphold its mission of fostering regional stability.

Eritrea, Somalia, and Egypt’s concerns over Ethiopia’s actions are converging. In August 2024, Egypt and Somalia signed a defense pact, under which Egypt deployed more than 5,000 troops to Somalia as part of the African Union peacekeeping mission, committed to joint military exercises, and supplied heavy weaponry, including rocket launchers and anti-tank systems. Both Hamza Hendawi and Kamal Tabikha, Cairo-based correspondents for The National, attributed this deepening of military ties in part due to shared regional worries over Ethiopia’s regional policy moves.

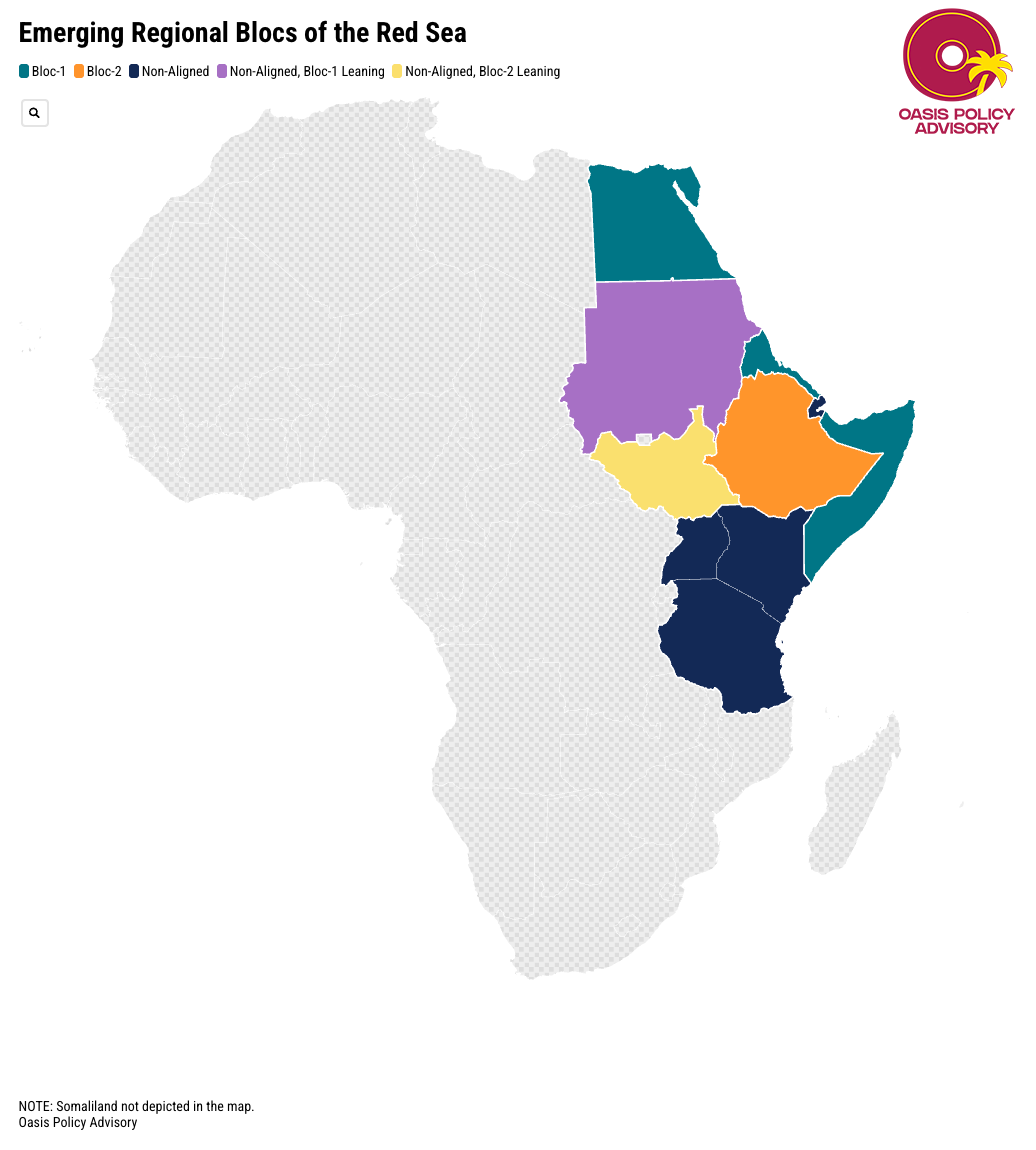

Connecting these developments reveals a broader shift: there is an emergence of two differing alignments in the Horn of Africa, with the Red Sea at the center of it.

This is where the investment calculus fundamentally changes. If these regional blocs solidify, they risk creating a proxy conflict environment where international actors support opposing regional states—such as the U.S. backing Eritrea and Russia backing Ethiopia—forcing foreign direct investment to follow suit. The recognition of Somaliland by Israel at the end of December has directed the Horn on this trajectory.

In this scenario, investment will mirror strategic alliances rather than pure market logic, as Western VC support aligns directly with foreign policy:

Bloc-Specific Due Diligence: Due diligence will pivot from analyzing consumer spending power to assessing the security guarantee of the host government and its foreign backers.

Port Politics: Ports become political instruments of influence. A VC-backed logistics firm in Djibouti, home to U.S., Chinese, and multiple European military bases, might find its market access restricted if it attempts to expand into a Bloc 2-aligned port like Somaliland’s Berbera.

Choking Capital Flows: While Western VC support in Ethiopia is rising (with firms like Unpopular Ventures and Partech Partners investing check sizes up to $60 million), rising Horn tensions could choke such heavy investments. This risk stems both from investor hesitancy over conflict and potential governmental pressure, pivoting capital toward more stable or allied countries.

Innovation on the Shores: Collapsing the Blue Economy Hedge

The stakes of this geopolitical crisis is the survival of the thriving, but vulnerable startup ecosystems dedicated to the blue economy in the region. Recent years have seen East Africa’s venture landscape vigorously focus on the sea, with Kenya at the core. The Western Indian Ocean Marine Science Association (WIOMSA) runs innovation funds providing grants of up to $200,000 to support new ventures.

Similarly, Pangea Accelerator, a joint Kenyan-Norwegian accelerator, has become one of the first blue‑economy accelerators operating in Africa, connecting regional startups with global investors focused on maritime trade. Likewise, Sote Hub, a startup support center in the Kenyan coastal city of Mombasa, is focused on nurturing ocean and inland‑water startups, aiding hundreds of MSMEs and high-potential ventures in blue economy, climate, and digital spaces.

And it’s not just Kenya. Seychelles issued the world’s first sovereign “blue bond” (backed by entities like Calvert Impact Capital), while pan-African enablers like OceanHub Africa (OHA) have backed 32 ocean-impact startups with over $10 million in external funding.

Africa’s overall bluetech sector, largely driven by innovators, is projected to be worth $1.5 trillion in revenue by 2050, contributing to over 51 million new jobs. But none of that can be realized if the region’s crises spiral along the Red Sea. It’s these small businesses and startup ventures that will be the greatest victims:

SME Vulnerability: Unlike large enterprises, which have the resources to maneuver such insecurity, SMEs lack the infrastructure to manage geopolitical risk, leaving them vulnerable to attacks on port facilities, supply chain disruption, and the deterrence of growth.

Foreign Funding Withdrawal: Startups rely heavily on foreign investment; 80% of Africa’s VC funding comes from North America and Europe. Foreign investors are far more likely to pull their support amid rising geopolitical risk, or else assign prohibitively high-risk premiums to venture debt, essentially cutting off access to growth capital.

Kenya’s Crumbling Neutrality: Failure of the Regional Anchor

For many VCs, Kenya—East Africa’s economic hub and startup funding leader—represents the strategic hedge, the stable anchor where regional operations can be safely headquartered. Increasingly, cleantech has become a rising sector for innovation in Africa, securing $192 million in equity funding in 2024, coming second to fintech. Paralleling this, Mombasa—Kenya’s coastal city—was ranked as the second strongest startup ecosystem in Kenya after Nairobi, showing over 100% annual growth in 2024.

However, Nairobi’s carefully calibrated neutrality is rapidly eroding, threatening its role as the regional blue-economy anchor and collapsing the portfolio diversification strategy for many Western funds, including those that could be directed to cleantech initiatives in Mombasa.

Nairobi maintains a delicate balance: it’s a strategic partner to Ethiopia (via the LAPSSET Corridor project) and maintains warm relations with Egypt (with trade peaking at $567 million in 2024). Yet, it has also entangled itself, having hosted a controversial summit for the RSF, which sparked international backlash and caused the SAF to recall its ambassador.

As tensions grow and amalgamate, Kenya’s ability to remain neutral is unlikely to last long, and its blue economy ventures will be among the first to feel it:

Limited Cross-Border Expansion: Heightened tensions between Ethiopia and Eritrea, for example, could exclude Kenyan SMEs from corridor-linked ports or preferential maritime logistic networks. Furthermore, access to regional expertise could be reduced as multi-country innovation clusters become politically-aligned hubs.

Financing & Risk Pricing: Insurers and financiers will assign higher country risk premiums to Kenyan ventures operating in politically sensitive zones or disputed waters. The result: higher costs for venture debt for blue economy projects, effectively increasing the barrier to scale.

Strategic Isolation Risk: If conflict or bloc competition escalates in the Red Sea corridor, Kenya’s lucrative ports may be bypassed for bloc-preferred logistics routes, shrinking business opportunities for port-adjacent ventures and challenging Nairobi’s role as the regional maritime gateway.

The Coming Red Sea Crunch

For over two years, the world has been fooled into thinking the Red Sea is just a Yemeni story. As with most global dynamics, there’s more than meets the eye.

The Horn of Africa is set to face turbulence for the years ahead. The war in Sudan continues to escalate; the gridlock between over the GERD intensifies; and Ethiopia’s relentless pursuit for the Red Sea is putting wood on an already strong fire.

All these tensions are slowly converging on the shores of the Red Sea. Yet this time, the burden will not be felt solely by the big maritime companies. It’s the small, innovative powers—the ones seeking to elevate East Africa’s seashore wealth—that will feel the pressure.

The endgame: the next shock to global trade and innovation will come out of a region everyone assumes is peripheral.

Oasis Media Collective goes where the headlines don’t by reporting on overlooked geopolitical dynamics. Follow for more to receive our data-driven storytelling and reporting.

Have questions or want to discuss opportunities directly? Connect with us here.