Is North Africa Becoming the World's Next Energy Bloc?

Libya's crude, Egypt's pipelines, and Algeria's gas are forming a Mediterranean energy corridor that the world is starting to notice

KEY FACTS

WHAT HAPPENED? The Iran energy crisis has pushed Egypt to import Libyan crude and accelerates North Africa's emergence as an alternative energy corridor

WHY IT MATTERS? Libya, Egypt, and Algeria are developing complementary energy roles, forming a functional Mediterranean energy system

WHAT’S NEXT? Whether this crisis-driven coordination hardens into durable integration depends on Libya's political stability and the Algeria-Morocco rivalry

For the Gulf, the closure of the Strait of Hormuz was a nightmare. For North Africa, it may be an opportunity.

As the primary export lane connecting GCC oil to global markets, the Hormuz’s closure disrupted critical energy supply chains, upending economies worldwide. But the redrawing of tanker routes has created an opening, and nowhere is that clearer than in North Africa.

The signal came from Cairo. Egypt’s state petroleum body announced it would import at least one million barrels per month of Libyan crude, a direct response to disrupted Kuwaiti supply flows cut off by the Hormuz blockade. While Egypt holds significant reserves—it’s Africa’s fourth-largest crude producer—its output has been declining, hovering around 507,000 barrels per day as of mid-2025, making it a net importer.

With Gulf oil temporarily off the table, the turn to Libya was logical. But it points to something larger: the early formation of a North African energy bloc.

Three Countries, Three Roles

Across North Africa, three countries are emerging as pillars of a wider regional energy transformation. Not through formal agreement, but through a natural and increasingly visible division of labor.

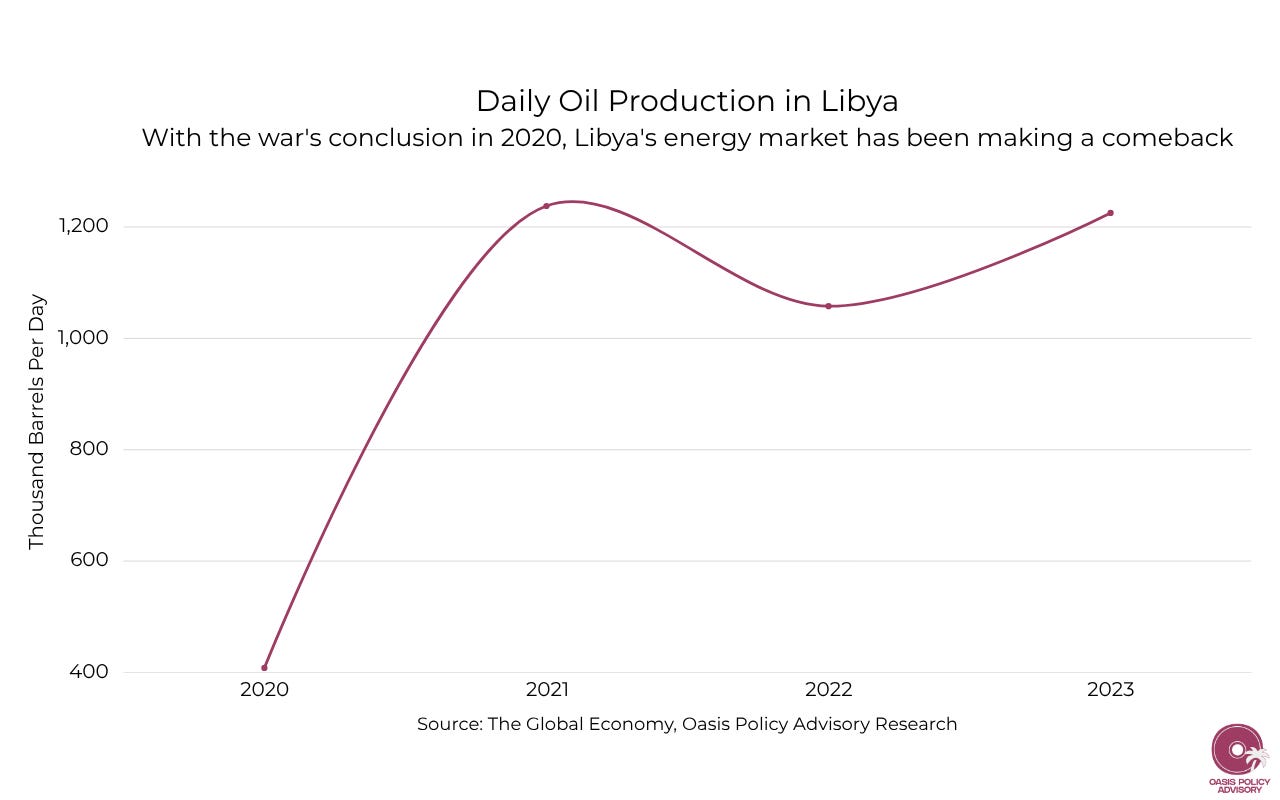

Libya is the crude supplier the region has long underused. Sitting on Africa’s largest reserves—48 billion barrels, ninth largest in the world—Libya was effectively shut out of global energy markets by a decade of civil war.

As it rebuilds, global energy giants have taken notice. TotalEnergies, ConocoPhillips, BP, and Shell have all signed exploration and redevelopment agreements with the Libyan National Oil Corporation (NOC), with combined commitments surpassing $20 billion. The NOC has set targets to raise production from 1.2 million bpd in 2025 to 1.8 million by 2027, with a long-term ambition of 2 million bpd.

Algeria, Africa’s second-largest oil producer, is the region’s gas pillar. With Europe’s energy supply disrupted by both the loss of Russian gas and now Gulf oil, Italy and Spain have turned to Algeria as a southern alternative. Via the TransMed and Medgaz pipelines, Algerian hydrocarbons are flowing into the EU at a scale that few anticipated even three years ago. Even with the Iran ceasefire, European dependence on Algeria is likely to deepen to avoid future shocks, paving the way for new long-term agreements.

Egypt, meanwhile, is not a dominant producer, but it may not need to be. It is already home to the SUMED pipeline, which carries close to 2.5 million bpd and moved 50 million tons of crude in 2025 alone.

Positioned between the Mediterranean and the Red Sea, Egypt serves as the connective tissue of the region: a transit and processing hub capable of routing oil from multiple sources to multiple markets. Ongoing economic reforms could strengthen that role further, positioning Egypt as a key exporter to northeast Africa and the Levant.

A Bloc by Function, Not by Name

The complementarity is real: one country supplies crude, one refines and routes it, one exports gas to the end market. That’s a supply chain, with or without a treaty.

But North Africa is not the GCC, and it would be premature to call it one. The energy infrastructure needed to cement the region as a leading global supplier is still developing, and given each country’s fiscal constraints, it will be built slowly. Most critically though: Geography is a strength; geopolitics remains a headwind.

Libya’s instability, persistent even after the civil war’s formal conclusion in 2020, threatens any long-term supply architecture. With the country still divided between the internationally recognized government and separatist forces, Libyan oil infrastructure is always at threat of being caught in the crosshairs.

The Algeria-Morocco rivalry is perhaps the most acute obstacle to wider Maghreb integration. Morocco, like Egypt, could serve as a key transit point for North African oil, but its dispute with Algeria over Western Sahara has already produced real consequences: In 2021, Algiers halted natural gas exports via the Maghreb-Europe pipeline running through Moroccan territory. That episode illustrates how easily the region’s energy potential buckles under political friction.

Why the World Is Watching

For European energy planners and investors, North Africa’s potential is no longer speculative. Algeria anchors southern pipeline supply; Egypt’s infrastructure offers a bypass lane for Gulf oil; Libya’s crude can reach Italian and Spanish refineries faster than almost any alternative.

This does not replace Gulf or Norwegian supply. But events unfold in the Gulf, the world will reassess its energy corridors. North Africa would do well to be ready when it does.

The region is not yet an energy bloc, but it may not need to be one to matter. What is forming is something more pragmatic: a crisis-tested Mediterranean energy system, built less by design than by necessity.

This reporting may be cited with attribution to Oasis Media Collective. For licensing, republication, or extended use, contact here.