How the Iran War Is Accelerating the Algeria and Morocco Rivalry

Because of the Gulf war, North Africa's two great rivals are racing to fill Europe's energy and trade void

KEY FACTS

WHAT HAPPENED? The Iran war is pushing Europe into its deepest energy and trade crisis since Russia's invasion of Ukraine

WHY IT MATTERS? Europe is turning to North Africa: Algeria for energy and Morocco for maritime trade

WHAT’S NEXT? Europe faces a structural choice: deepen dependence on Algerian gas via expanded pipeline deals, double down on Moroccan logistics as a rerouting hub, or accept that both relationships carry their own geopolitical risks

European markets are rattled. Following President Donald Trump’s televised threat to bomb Iran “back to the Stone Ages,” crude oil has surged from roughly $102 to a high of $112 a barrel. The market turbulence is straining Washington’s already-fraught relations with Europe: Trump’s war of words with French President Emmanuel Macron, who publicly criticized the Iran war, is the sharpest symbol of a transatlantic alliance under pressure.

With oil markets in turmoil and the Strait of Hormuz closed, European investors are confronting a familiar question in an unfamiliar form: where does the continent turn when its energy corridors go dark? Increasingly, the answer runs through North Africa, and through two neighboring rivals with very different things to offer.

Africa’s Sleeping Energy Giant Wakes Up

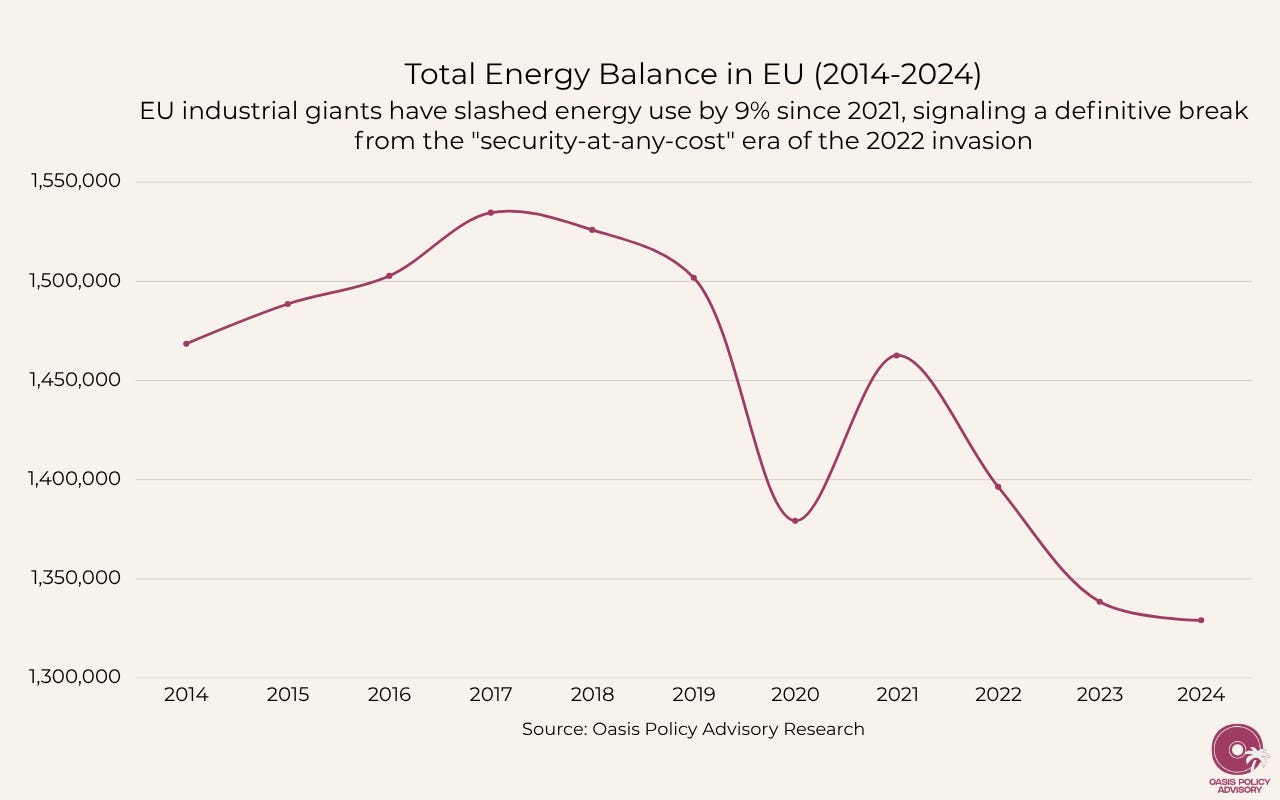

Europe entered the Iran crisis badly exposed. Gas storage was already running 35% below the five-year average, leaving almost no cushion against supply shocks. It’s here that Algeria goes from being important to becoming indispensable.

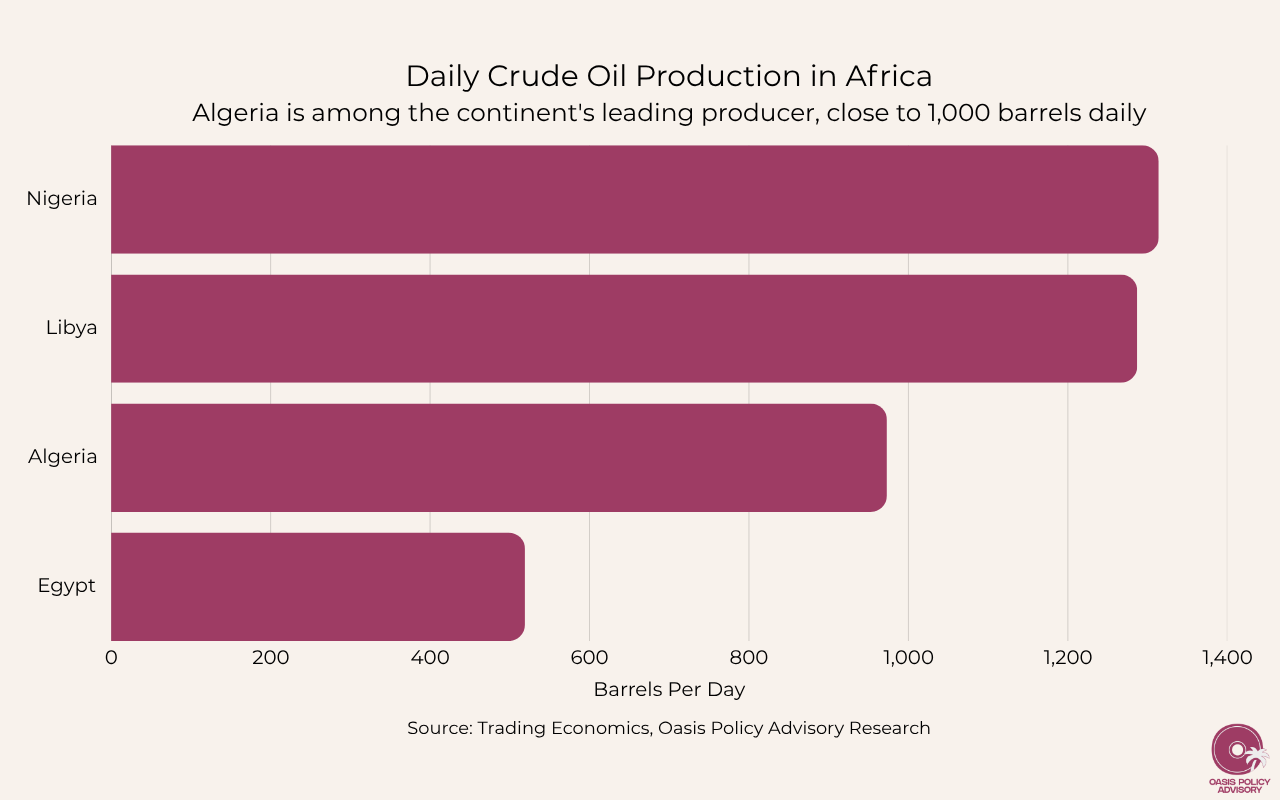

As Africa’s third-largest holder of oil reserves and among its leading producers at roughly 1.2 million barrels per day, Algeria exported 39.2 billion cubic meters of gas to the EU in 2024, approximately 14-15% of the bloc’s total imports, making it Europe’s fourth-largest supplier behind Norway, Russia, and the United States.

For Spain, the dependence is acute. Algerian gas accounted for more than 29% of Spanish imports in January and February according to Reuters, and Madrid is now in active talks with Algiers about expanding Medgaz pipeline capacity by up to 10%. Italy is moving in the same direction: Algeria already supplies 30% of Italy’s gas, a share likely to grow as the two countries negotiate expanded volumes and new upstream projects.

Algeria cannot instantly flood Europe with unlimited gas; pipeline capacity and upstream investment remain real constraints. But the strategic logic is compelling. Every percentage point of Hormuz risk makes Algerian pipeline gas more valuable precisely because it bypasses maritime chokepoints entirely.

The Kingdom at the Crossroads

The Hormuz closure is only part of Europe’s maritime headache. Iran-backed Houthi forces are raising the specter of a renewed Red Sea blockade, a corridor through which 12% of global trade flows. Key commodities, from coffee to tea, face supply chain disruption at a moment when Europe can least afford it.

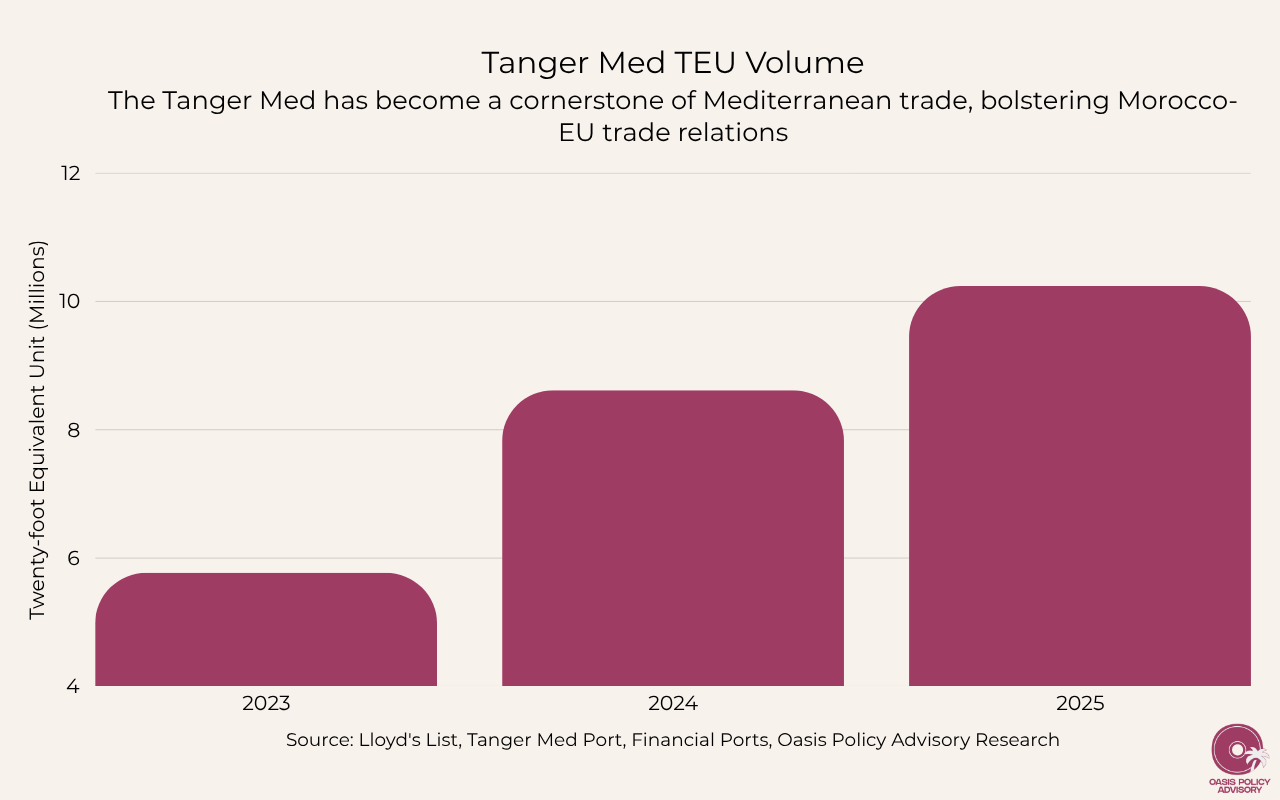

This is Morocco’s opening. Rather than energy, Morocco is positioning itself as Europe’s indispensable logistics partner when shipping lanes become unreliable. Tanger Med, the Kingdom’s flagship industrial port complex, handled 10.24 million TEUs and 142 million tonnes of cargo in 2024, cementing its place as one of the Mediterranean’s leading container hubs. Its rise was already accelerated by the earlier Red Sea crisis, as shipping companies rerouting around South Africa found Tanger Med a natural convergence point at the Atlantic-Mediterranean junction.

The trade numbers reflect this deepening relationship. EU-Morocco trade exceeded €60 billion ($69 billion) in 2024—a 7% increase from 2023—with the EU absorbing roughly two-thirds of Moroccan exports. Brussels designated Morocco a “crucial trading partner” last April. Vehicle exports alone tell part of the story: nearly 540,000 finished cars shipped from Tanger Med to Europe in 2024. With companies like Maersk now avoiding the Red Sea, that volume is set to climb further.

Old Rivals, New Stakes

Underneath the opportunity lies a long and unresolved rivalry. In 2021, Algiers halted natural gas exports via the Maghreb-Europe pipeline transiting Moroccan territory, weaponizing infrastructure amid escalating tensions over Western Sahara. The closure was a statement as much as a decision: Algeria would not allow Morocco to benefit from its energy exports, even indirectly.

The Iran crisis intensifies that dynamic. Algeria can double down on its energy edge: expanding pipelines, negotiating new volumes, and deepening bilateral ties with Spain and Italy. Morocco, lacking Algeria’s energy reserves, responds by leveraging its geographic proximity to Europe and its expanding port infrastructure to lock in its role as the continent’s trade facilitator. Both countries grow more important to Europe in parallel, and by extension, their rivalry deepens.

For European investors, this is where opportunity shades into risk. Algeria’s gas leverage cuts both ways: Algiers can restrict supply as easily as it expands it, as 2021 demonstrated. Morocco’s supply chain integration is real, but still maturing. The continent needs both Algeria’s molecules and Morocco’s logistics, and dependence on each carries its own political price.

The Iran crisis is accelerating a realignment that was already underway. The lesson for Europe is that energy security and supply-chain resilience are now inseparable, and that both increasingly run through a stretch of coastline the continent has long underestimated.

This reporting may be cited with attribution to Oasis Media Collective. For licensing, republication, or extended use, contact here.