Why Europe's Energy Crisis Just Got Dramatically Worse: Gulf Crisis and the Red Sea

Expected Houthi resumption of Red Sea attacks is pushing European energy markets toward their most precarious moment since 2021

KEY FACTS

WHAT HAPPENED? Coordinated US-Israeli strikes on Iran have pushed pushed Brent crude up 13%, as Tehran and its allies threaten pressure on the Strait of Hormuz and Red Sea

WHY IT MATTERS? Europe has become deeply reliant on Gulf oil and any disruptions in the Red Sea will only further strangle the continent’s energy supply chains

WHAT’S NEXT? European nations may deploy naval forces to protect the Red Sea while deepening economic engagement with South Africa

What Happened

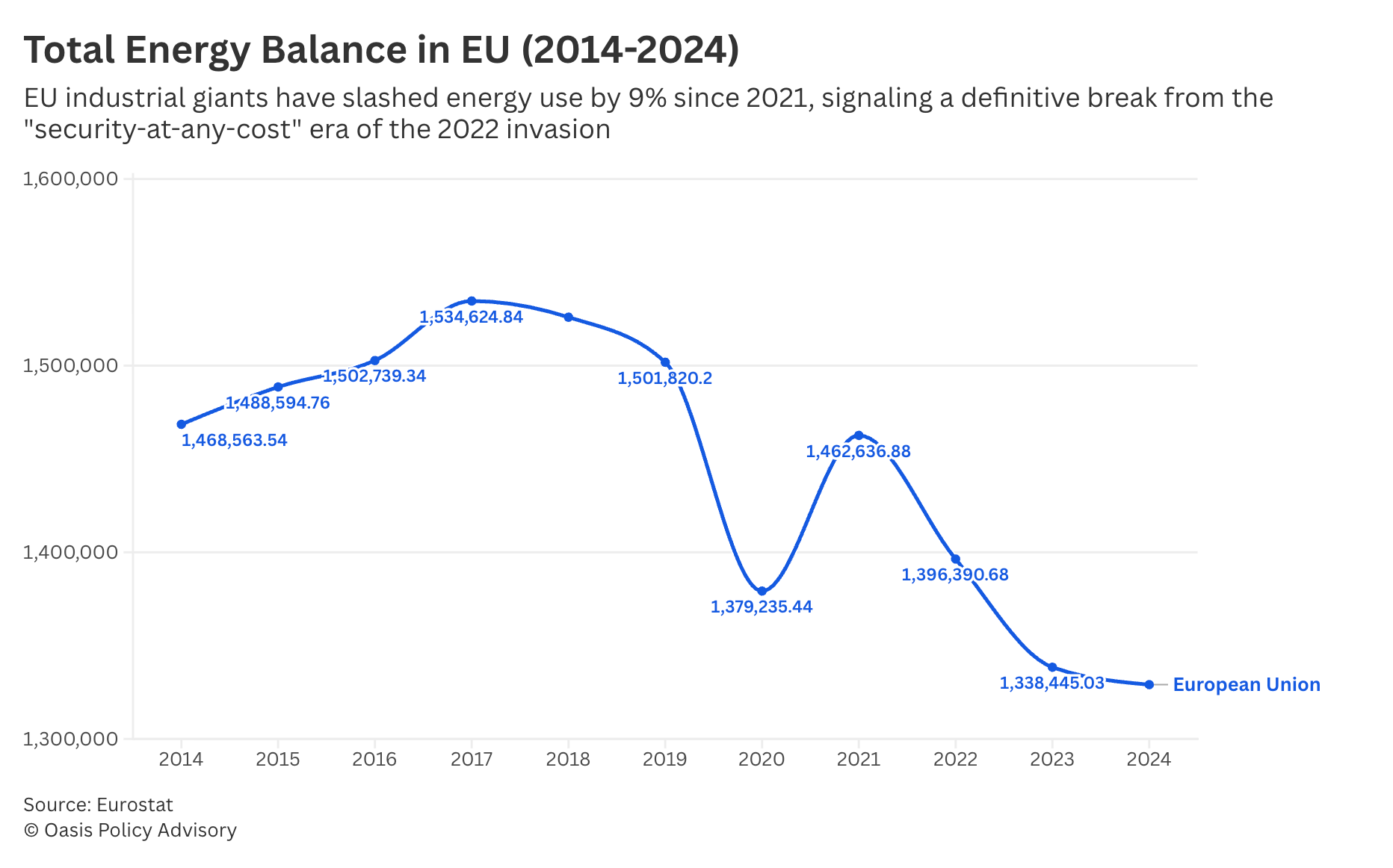

Europe’s ongoing energy crisis is set to face deeper turbulence. With the continent’s energy balances down roughly 9% since 2021, the EU has relied increasingly on Gulf oil to meet its energy needs, yet that reliance has become a hindrance amid the ongoing Middle East crisis. This weekend, coordinated strikes by the United States and Israel killed Iran’s top leadership, prompting Tehran to retaliate across the Gulf.

The region finds itself teetering toward chaos, with oil markets following suit. The significant variable in this calculus is the Strait of Hormuz, a critical chokepoint through which a fifth of the world’s oil is transported. The Strait is currently facing pressure as Iran threatens to close it; that threat alone has sent Brent crude oil prices flying by 13% to $22 a barrel, while shipping giants such as Danish Maersk have suspended vessel crossings in the Strait.

Yet, as Middle East analyst of The Levant Lens, Bassel Doueik, notes, the Hormuz is only one part of the wider passageway through which Gulf oil is transported to Europe.

“We often think the Strait of Hormuz is the only corridor to watch for oil trade routes to Europe, but the Red Sea has been under sustained pressure from Houthi militias in Yemen since 2023,” Doueik said. “If attacks resume, it could strangle the trade route to the European Union and spike oil prices further.”

Why It Matters

The last Houthi campaign in the Red Sea—which the group announced it intends to resume—sparked a 30% rise in container freight rates and an average two-week increase in shipping time. Already, Maersk announced it would also pause traversals in the Red Sea, and other shippers are likely to follow suit.

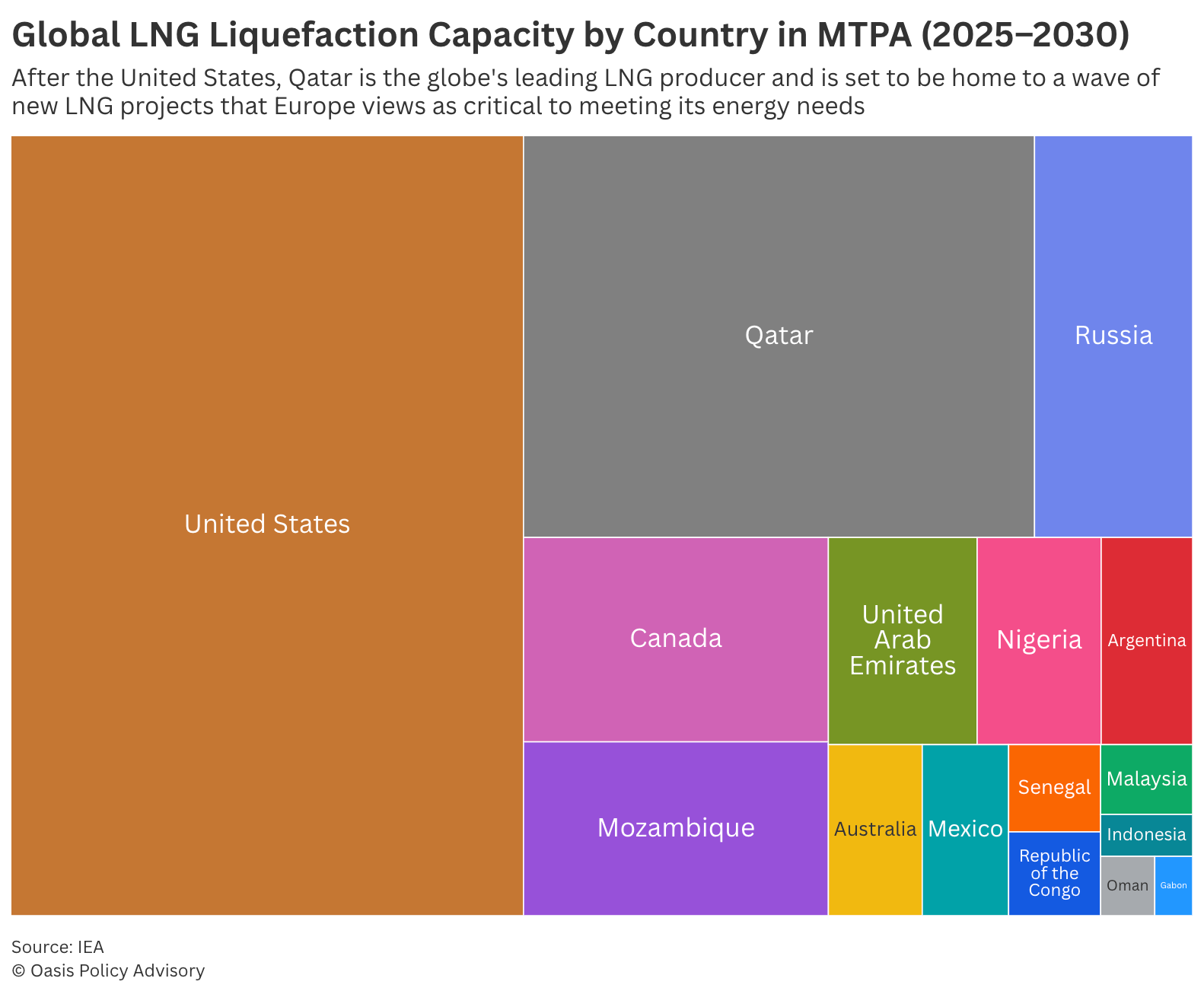

The result will only strangle Europe’s energy supply even more. QatarEnergy, one of the globe’s most prominent energy suppliers, has paused LNG production operations amid the conflict, increasing natural gas prices across Europe and Asia by 30%. The pause of operations by shippers such as Maersk will only spike prices further as supply limits.

“With Maersk suspending operations, this is a big hit for the entire world,” Doueik said. “Shipping costs rise, oil prices rise, and living costs in Europe increase.”

The move is particularly concerning as the continent enters the spring and summer months, increasing consumer demand for air conditioning.

What’s Next

The coming weeks will be decisive. During the Houthis’ last campaign, various European countries took part in Operation Prosperity Guardian, a multinational coalition to counter the Houthis attacks. Doueik suggests we could see something similar unfold.

“If supply shortages are detected, European countries may even deploy naval units to ensure ships can transit safely,” Doueik said. “A French aircraft carrier has already been deployed to the Middle East, signaling anticipation of increased attacks.”

While shippers such as Maersk have announced their intention to revert their Red Sea shipments southward along the Cape of Good Hope, even this isn’t enough to address concerns. Not only will it likely add over ten days of traversal to European markets, but South Africa’s increasing alignment with BRICS has become a geopolitical flashpoint between Pretoria and the West. South Africa’s recent condemnation of the American and Israeli strikes—which the EU has largely supported—may spark frictions that slow down this traversal lane, such as the implementation of sanctions targeting South African ports along the Cape.

“The Red Sea is another pressure point that could strangle trade routes to Europe,” Doueik said. “Combined with Gulf instability, it heightens the risk to European energy markets and living costs.”

This reporting may be cited with attribution to Oasis Media Collective. For licensing, republication, or extended use, contact here.

The important point here is that Europe’s exposure isn’t just to higher oil prices — it’s to the compression of transport routes at both ends of the chain. If Hormuz threatens upstream flows while the Red Sea disrupts downstream transit, the issue becomes less about replacing barrels and more about how quickly energy, LNG, and refined products can actually move into European markets.

That’s where the deeper stress emerges: insurance premia, rerouting delays, freight costs, and refinery economics begin tightening before any formal shortage appears. Europe’s energy vulnerability is no longer just about import dependence; it’s about whether multiple chokepoints start reinforcing each other at the same time.

Europe’s vulnerability here isn’t just about the Red Sea or Hormuz individually—it’s about the compounding effect of chokepoints across the same supply chain.

After 2022, Europe replaced pipeline dependence with maritime dependence. That shift looked like diversification on paper, but in practice it concentrated risk along a handful of sea lanes—Hormuz, Bab el-Mandeb, and the Suez corridor.

If pressure emerges across multiple points simultaneously, the issue stops being an energy shock and starts looking like a systemic logistics shock. And those tend to cascade far beyond energy markets into inflation, industrial output, and political stability.

The real question is whether Europe is prepared for persistent disruption rather than temporary crises.