Ghana Just Rewrote the Rules of Gold. The World Should Pay Attention

As gold surges past $5,000 an ounce, Ghana has quietly restructured its mining royalty system, with consequences that stretch far beyond West Africa

KEY FACTS

WHAT HAPPENED? Ghana replaced its flat 5% gold royalty with a price-linked sliding scale of 5-12%

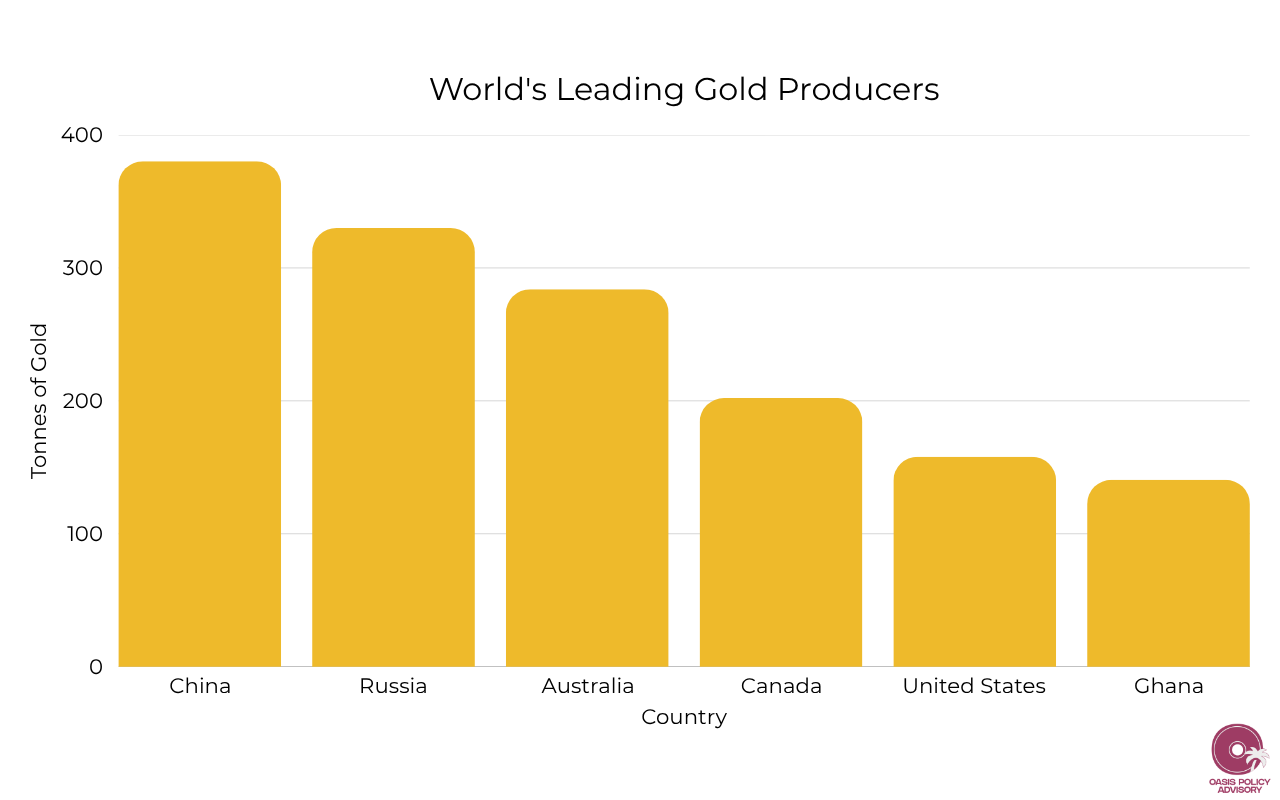

WHY IT MATTERS? Ghana is Africa’s largest and the world’s sixth largest gold producer, and the reform has drawn rare joint opposition from the US and China, signaling that what happens in Accra doesn’t stay in Accra

WHAT’S NEXT? If Ghana’s royalty overhaul proves lucrative, it’s likely to accelerate a broader wave of resource nationalism across Africa

Gold prices have been hitting historic highs, trading above $5,000 an ounce. Even after facing a sharp fall earlier in March, rates for gold are now seeing a comeback.

With the Iran war threatening the global economy, investors are fleeing to safe-haven assets, chief among them gold. Yet unbeknownst to them, one of the world’s most important gold hubs just rewrote the rules of the game.

Ghana is not only Africa’s largest gold producer, but the sixth largest in the world, producing roughly 140 tonnes annually. Effective this month, Accra replaced its flat 5% royalty fee with a price-linked sliding scale of 5-12%.

While primarily a domestic fiscal move, the reform’s effects are likely to ripple into investment flows, supply chains, and commodity markets in the long term. Already, world powers such as the US and China—competitors for influence in Africa—have both voiced their opposition to the policy, along with other countries, signaling the geopolitical stakes.

A Gold Rush Dividend

For decades, producers tapping into Ghana’s vast gold wealth were subject to a flat 5% royalty on gross revenue. 2025, however, saw the introduction of a new regime created by the Minerals and Mining Royalty Regulations.

The regulations introduce variable royalty bands for gold, lithium, and selected minerals, with rates adjusting automatically to international prices. For gold specifically, the rate is pegged between 5% and 12%, with the top rate activated when gold exceeds $4,500 per ounce.

The royalty aims to leverage higher gold prices for Ghana, already a key economic pillar for the country. The Minerals Income Investment Fund reported that mineral royalty receipts reached a record high of GHS 5.43 billion (~$494 million) in 2025, up 10.8% from GHS 4.90 billion (~$446 million) in 2024. With J.P. Morgan predicting spot gold prices to potentially surpass $6,000 an ounce in the long term, the sliding scale aims to capture more revenue during high-price cycles without deterring investment when prices are low, a rules-based alternative to a windfall tax.

With gold demand spiking, so too does the demand for Ghanaian gold production. Yet as the mineral 9is already above $5,000 an ounce, the top band of Ghana’s new fiscal regime is immediately operative for any new operations.

Ghana produced roughly 4.9 million ounces of gold in 2024, according to the International Trade Administration. That marked an 8.5% year-on-year increase, and a moderate royalty hike is unlikely to reverse this momentum in the short run.

Yet in the long term, mining companies could gradually shift exploration capital toward other African nations to avoid incurring steeper costs. While fellow West African nations such as Mali are likewise rich in gold, the country’s ongoing conflict heightens security risks for production.

Rather, mining companies would more likely shift capital to Southern Africa, where countries such as South Africa are home to numerous gold mines. Yet even Southern Africa remains risky; the region continues to struggle with illegal mining operations that threaten long-term production and export projects.

Critically, Ghana is far from the only African gold producer to flirt with a royalty-scaling regime. Last November, Zimbabwe, the eighth largest producer on the continent, formulated a new revenue policy in which miners are required to pay a 10% royalty when prices exceed $2,501.

If gold prices continue to surge and Ghana accrues significant revenues as a result of its fiscal program, other states across the continent are likely to follow suit.

Global Ripple Effects

Ghana represents a mid-single-digit share of global mine supply. Its royalty change alone is unlikely to structurally move global prices, which remain driven by real interest rates, dollar dynamics, and geopolitical risk.

Yet the cost-curve effect is undeniably there, though its full weight may take years to materialize. A higher fiscal take does nudge Ghana’s all-in sustaining costs upward, marginally steepening the global cost curve over time, especially if neighboring countries develop similar policies.

Producers facing steeper marginal royalties at higher prices may be incentivized to increase forward contracts to lock in cash flows, adding incremental selling pressure in futures markets.

In that regard, Ghana’s sliding-scale royalty is a calibrated bet: capturing more upside from a historic gold price rally while attempting to preserve long-term competitiveness.

For investors, miners, and policymakers looking from the outside, it signals a broader African trend toward resource nationalism: Where the state is rewarded more generously in exchange for greater international supply access. And from that angle, this trend may not be Africa-exclusive for long.

This reporting may be cited with attribution to Oasis Media Collective. For licensing, republication, or extended use, contact here.